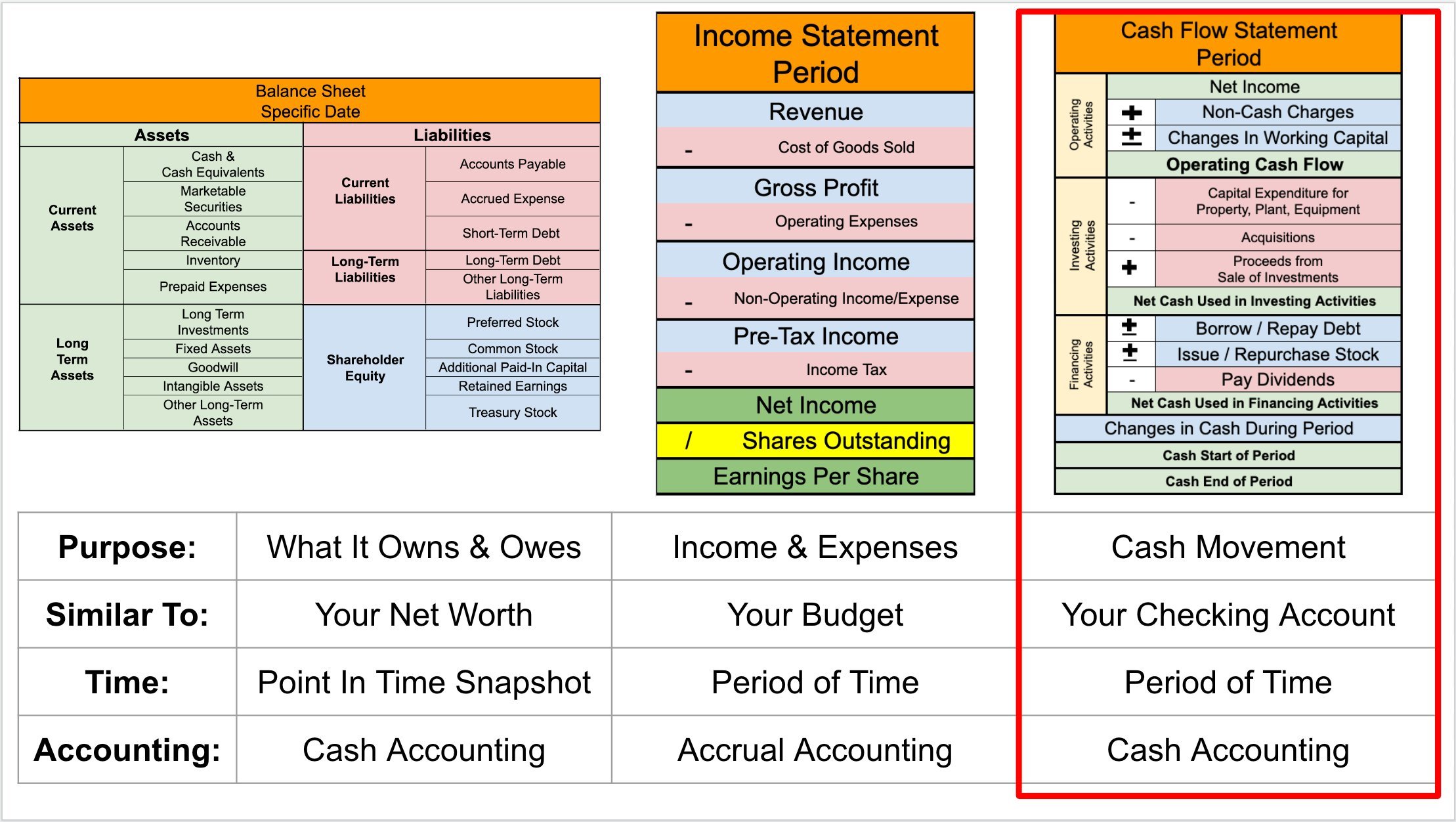

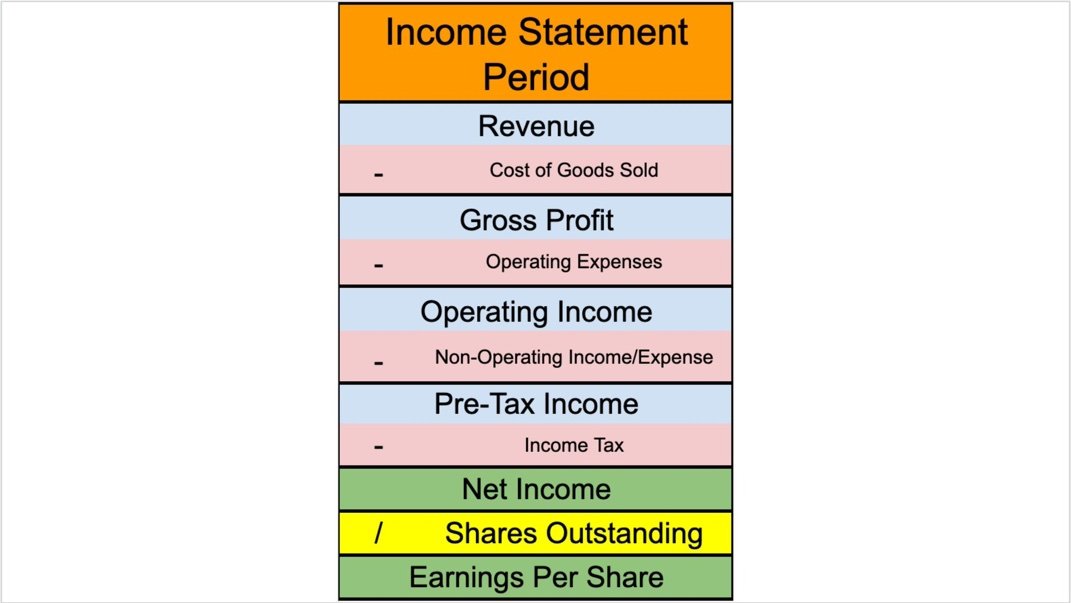

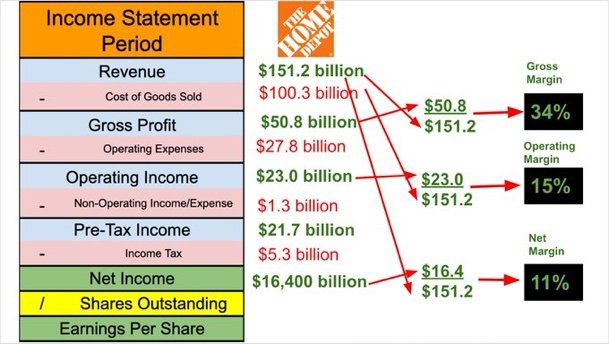

The top of this table will always be “Net Revenue” (Total Sales) during the period shown. When folks say “top line revenue” they truly mean the revenue from the top line of your Income Statement. As we move down the Income Statement we subtract expense by expense until we get to Net Income.

The first expense is the Cost of Good Sold (also called the Cost of Sales). The “Cost of goods sold (COGS) refers to the direct costs of producing the goods sold by a company.” As such manufacturing companies will usually have a much higher COGS than service companies.

Gross Profit (also called Gross Income) is the total profit after accounting for the direct costs of selling the goods your business makes, but calling it profit seems misleading because there are still a bunch of very real expenses that your business has to cover.

Operating Expenses are the total expenses required to operate your business (sometimes these are spilt out into categories including selling, general and administrative expenses, research and development expenses, depreciation and amortization, etc). When Operating Expenses are removed from Gross Profit, you have Operating Income (sometimes called EBIT = Earnings Before Interest and Taxes).

Non-Operating Income is most commonly interest that you pay to someone else or interest that is paid to you (investment income is also recorded here). For most small businesses the difference between Operating Income and Pre-Tax Income is small. A good CFO can significantly enhance Non-Operating Income! Pre-Tax income is also called Earnings Before Tax.

Normalizing your financial metrics helps benchmark your business against your peers. The most common